Let’s imagine a giant, glowing price tag hovering over a quintessential American neighborhood. On it, etched in bold letters, are the components of today’s American Dream:

HOME OWNERSHIP: $374,900

HEALTHCARE: $22,221/year

COLLEGE EDUCATION: $103,456

RETIREMENT: $1,120,000

WORK-LIFE BALANCE: PRICELESS

Staggering, isn’t it? The cost of the American Dream has skyrocketed, leaving many wondering if it’s still attainable. As a result, employee benefits have become the unsung hero of the modern workforce.

Think of benefits as a bulk discount on life’s essentials. They’re the invisible force that makes the dream more accessible. In fact, 96% of Americans believe it is the employer’s responsibility to offer health insurance. It’s no small change either – the U.S. employee benefits market was valued at a whopping $1.7 trillion in 2020.

But here’s the kicker – benefits aren’t just extras. They’re a substantial part of your compensation. On average, they account for 31% of the average American pay cheque. That’s right – nearly a third of your earnings might be hiding in plain sight.

From the birth of Social Security to the rise of 401(k)s, from health insurance to wellness programs, the story of employee benefits is the story of the American workforce. It’s a tale of adaptation, innovation, and at times, heated debate.

And the impact? It’s deeply personal. Just ask the young graduate choosing a job based on student loan assistance, or the parent relying on employer-sponsored childcare.

The Birth of America’s Employee Benefits Safety Net

In the dawn of the 20th century, the American workplace was a far cry from what we know today. On a typical factory floor in 1900, the air was thick with smoke and the deafening roar of machinery never ceased. Workers, many of them children, toiled for 12 to 14 hours a day, six or seven days a week. Safety regulations? Nonexistent.

The human cost was staggering. In 1913, the U.S. Bureau of Labor Statistics reported 23,000 work-related deaths among a workforce of 38 million. To put this in perspective, that’s equivalent to 165,000 deaths in today’s workforce – more than all U.S. military casualties in World War I.

But amid this grim landscape, a few forward-thinking companies were planting the seeds of change. The concept of “welfare capitalism” emerged, with some employers offering rudimentary benefits to workers. The Pullman Company, for instance, built entire towns for its employees, complete with housing, schools, and hospitals.

The Great Depression

The stock market crash of 1929 plunged America into its deepest economic crisis. By 1933, unemployment had skyrocketed to 24.9%, and half of the nation’s banks had failed. Millions of Americans faced destitution in their old age, with no safety net to catch them.

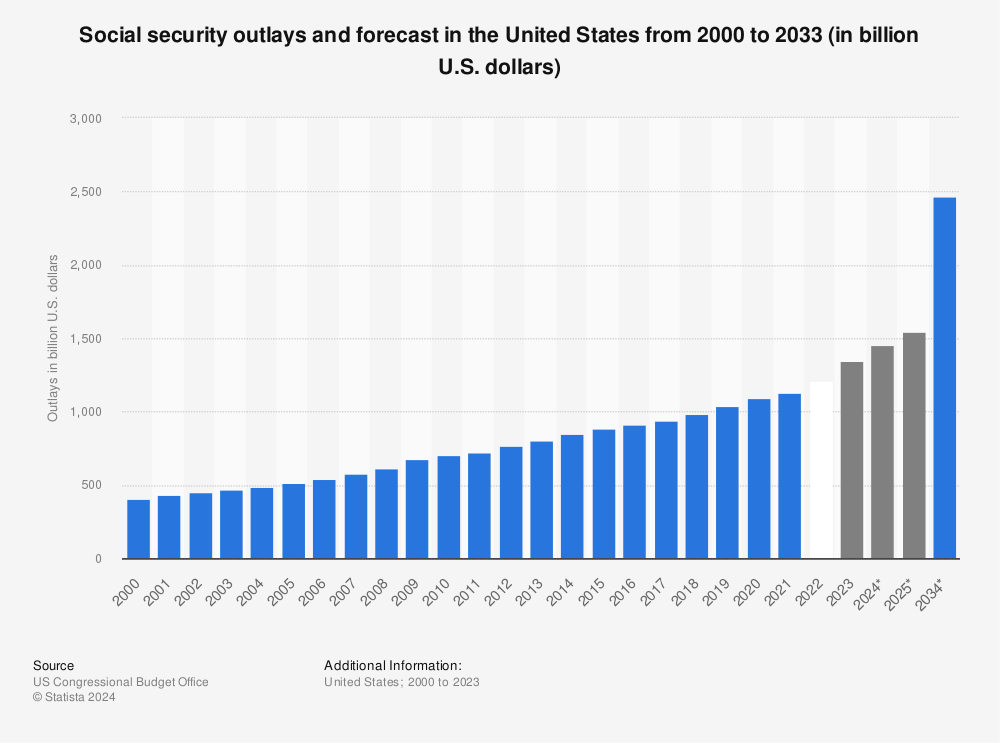

It was against this backdrop that one of the most significant pieces of social legislation in American history was born: The Social Security Act of 1935. For the first time, the federal government took on the responsibility of providing old-age insurance and unemployment benefits. The initial Social Security tax rate was set at a modest 2%, split evenly between employee and employer.

The impact was immediate and profound. By 1940, just five years after the Act’s passage, 222,488 Americans were receiving Social Security benefits. Today, that number has grown to over 66 million.

The initial exclusion of agricultural and domestic workers – who were disproportionately minorities – sparked heated debate. This early policy decision would have long-lasting effects on wealth inequality in America. Moreover, the very idea of government involvement in retirement security was hotly contested, a debate that continues to this day.

World War II: The Accidental Birth of Employer-Sponsored Health Insurance

As America mobilized for war in the early 1940s, the government imposed strict controls on the economy to prevent inflation. The 1942 Stabilization Act froze wages, leaving employers in a bind: How could they attract and retain workers in a tight labor market without raising salaries?

The answer came in the form of benefits. In 1943, the Internal Revenue Service made a crucial ruling: employer-provided health insurance would be tax-free. This seemingly minor tax decision would reshape the American healthcare landscape for generations to come.

The results were dramatic. In 1940, only 9% of Americans had employment-based health insurance. By 1950, that number had soared to over 50%. One early adopter of this trend was Kaiser Shipyards, which offered comprehensive health coverage to its workers. This model would later evolve into Kaiser Permanente, one of the largest healthcare providers in the country.

The Post-War Boom

The 1950s ushered in an era of unprecedented prosperity. GDP growth averaged over 4% annually, and unemployment held steady at around 4.5%. With this economic security came a rapid expansion of employee benefits.

Private pension plans, once a rarity, became increasingly common. In 1940, just 3.7 million workers were covered by such plans. By 1960, that number had ballooned to 19 million. This growth was driven by a combination of factors: strong unions, tax incentives, and companies eager to attract and retain skilled workers in a competitive job market.

The government also played a role in cementing the importance of benefits. The Welfare and Pension Plans Disclosure Act of 1958 established reporting requirements for employee benefit plans, while the Federal Employees Health Benefits Program of 1959 provided comprehensive health coverage for government workers.

By 1965, employer-provided health coverage had become the norm, with 70% of workers covered. However, this system had a significant downside: those without stable employment – including part-time workers, the unemployed, and retirees – were often left without coverage.

The concept of “fringe benefits” took hold during this period. Paid vacation time, life insurance, and disability coverage became increasingly common.

The First Signs of Trouble

As the 1960s dawned, healthcare costs, which had remained relatively stable for decades, started to rise sharply. Hospital expenditures nearly doubled between 1960 and 1965, jumping from $9 billion to $14 billion.

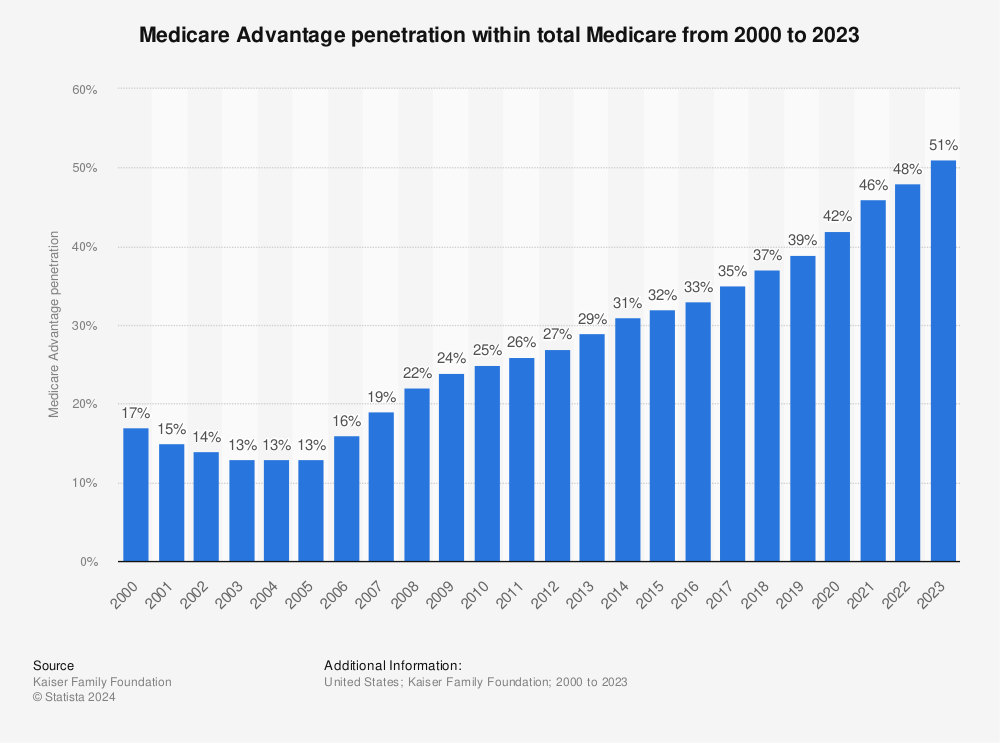

In 1965, President Lyndon B. Johnson signed Medicare and Medicaid into law in response to growing concerns about healthcare access for the elderly and the poor. The initial Medicare Part A premium was set at just $3 per month, a figure that seems quaint by today’s standards.

Yet even as these programs expanded coverage, they also contributed to rising costs. National health expenditures as a percentage of GDP rose from 5.0% in 1960 to 6.2% in 1965. This upward trend would accelerate in the coming decades, reaching 19.7% by 2020.

1974 ushered in a new era with the Employee Retirement Income Security Act (ERISA). Before ERISA, only half of pension participants ever saw a dime. After? A boom in pension plans – from 311,000 in 1975 to 713,000 by 1980.

ERISA also birthed the Pension Benefit Guaranty Corporation. Initial premium: a mere $1 per participant per year. Little did anyone know how crucial this safety net would become.

1985 brought COBRA, offering continued health coverage for job changers and the newly unemployed. The catch? In 2021, the average monthly COBRA premium for a family hit $1,812. A steep price for peace of mind.

in 1978, What started as an obscure tax provision became a retirement revolution. Johnson & Johnson pioneered the first 401(k) in 1981. By 1990, 19.5 million Americans were enrolled.

But this shift came at a cost. In 1975, 88% of private sector workers with pensions had guaranteed benefits. By 2018, only 33% did. The rest? Left to navigate the unpredictable waters of the stock market. The late ’70s introduced cafeteria plans, allowing employees to customize their benefits.

As healthcare costs ballooned, a new solution emerged: managed care. HMOs and PPOs promised cost control. By 1993, 51% of workers were enrolled. But with control came controversy – restricted choice and denied care sparked a backlash.

The ACA Revolution

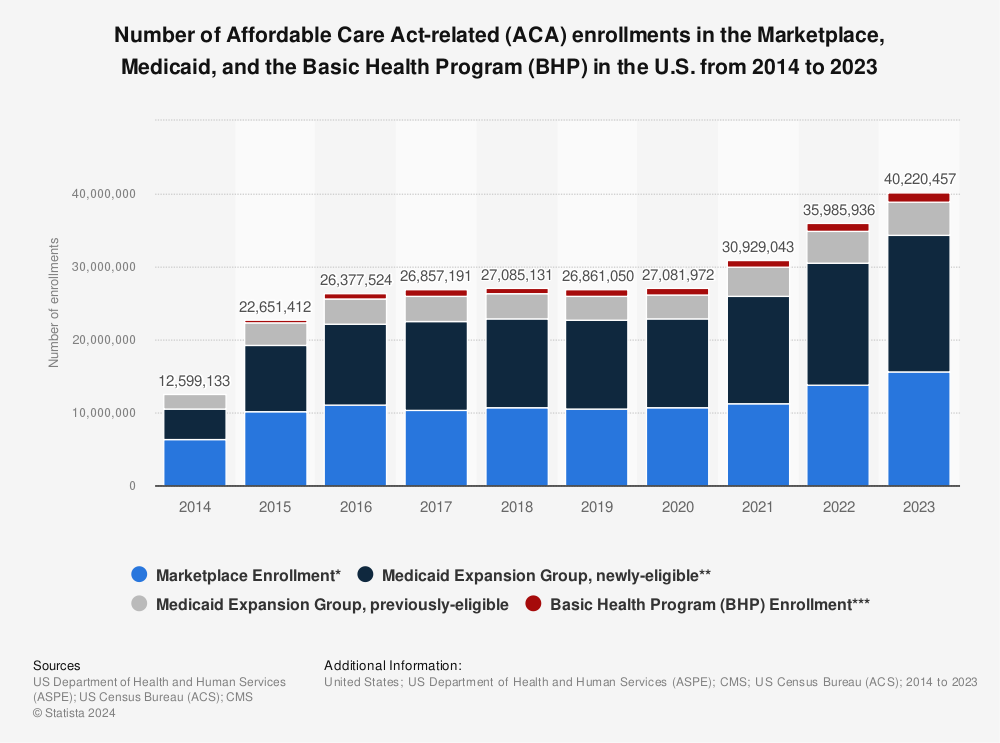

The Affordable Care Act of 2010 reshaped the healthcare landscape. Its key provisions – the individual mandate, employer mandate, and essential health benefits – aimed to expand coverage and improve care.

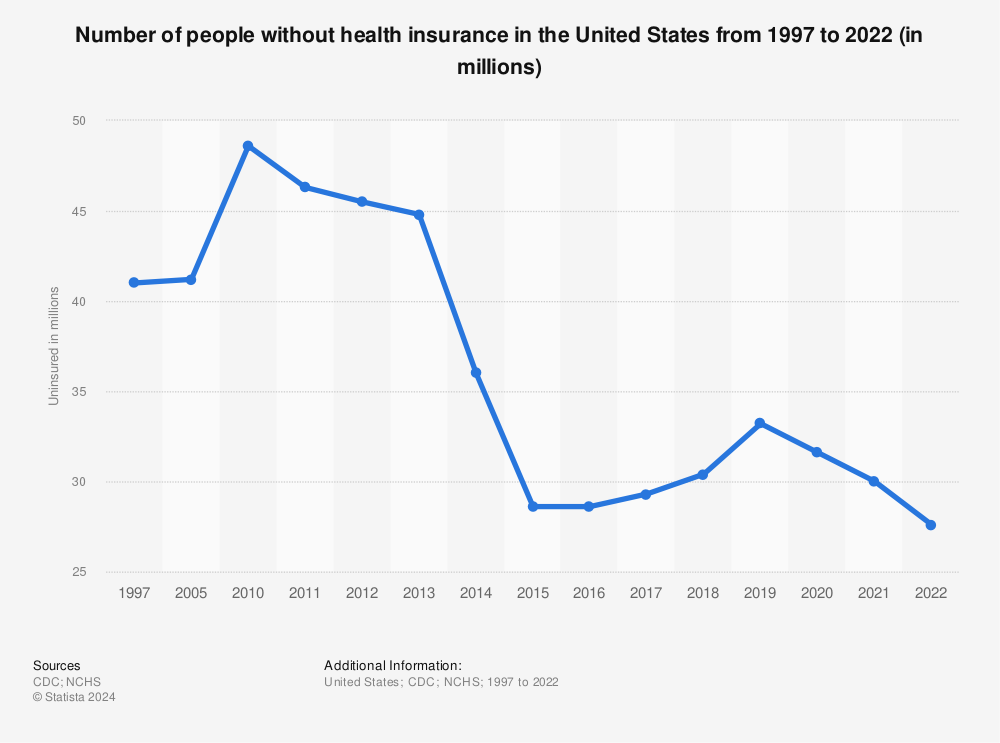

The impact was significant. The uninsured rate dropped from 15.5% in 2010 to 8.6% in 2021. Millions of Americans, many for the first time, had access to comprehensive health coverage.

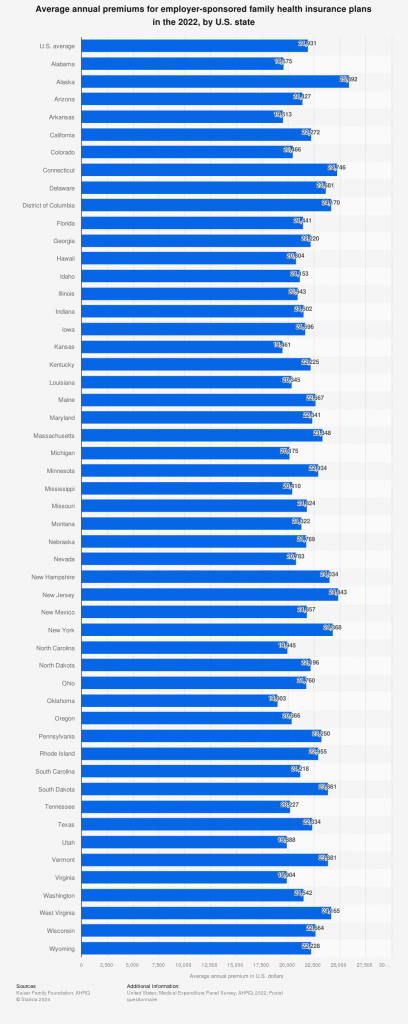

But this expanded coverage came at a cost. In 2021, average annual premiums for employer-sponsored health insurance reached $7,739 for single coverage and $22,221 for family coverage. These figures represent a significant portion of total compensation, straining both employer budgets and employee wallets.

The proposed “Cadillac Tax” on high-cost health plans, though ultimately repealed, sent benefit designers scrambling. Many employers redesigned their health plans, often shifting more costs to employees through higher deductibles and co-pays.

Navigating the Modern U.S. Benefits Maze

High-deductible health plan or traditional? How much should someone contribute to their 401(k)? What about that new critical illness insurance? Each choice feels like a high-stakes gamble.

By 2027, gig workers are expected to make up 50% of the US workforce. This shift promises flexibility and autonomy, but it comes with a significant downside: only 40% of gig workers have access to employer-sponsored health insurance.

Mental Health: No Longer Taboo

If there’s a silver lining to the COVID-19 pandemic, it’s the increased focus on mental health. The collective trauma of lockdowns, health fears, and economic uncertainty brought mental well-being to the forefront of the benefits conversation.

This shift manifested in various ways:

- Expanded Employee Assistance Programs (EAPs), offering more free counseling sessions.

- Addition of mental health apps like Calm or Headspace to benefits packages.

- Training for managers in recognizing and responding to mental health issues.

Perhaps the most dramatic change was the explosion of telehealth, particularly for mental health services.

However, as these programs grow more sophisticated, questions of privacy and fairness have emerged. How much health data should employees be expected to share? Do these programs inadvertently discriminate against certain groups?

Union workers are 26% more likely to have employer-provided health insurance compared to their non-union counterparts. The difference in retirement benefits is even more stark: 96% of union workers have access to retirement benefits, compared to only 69% of non-union workers.

Executive Compensation: The Widening Gulf

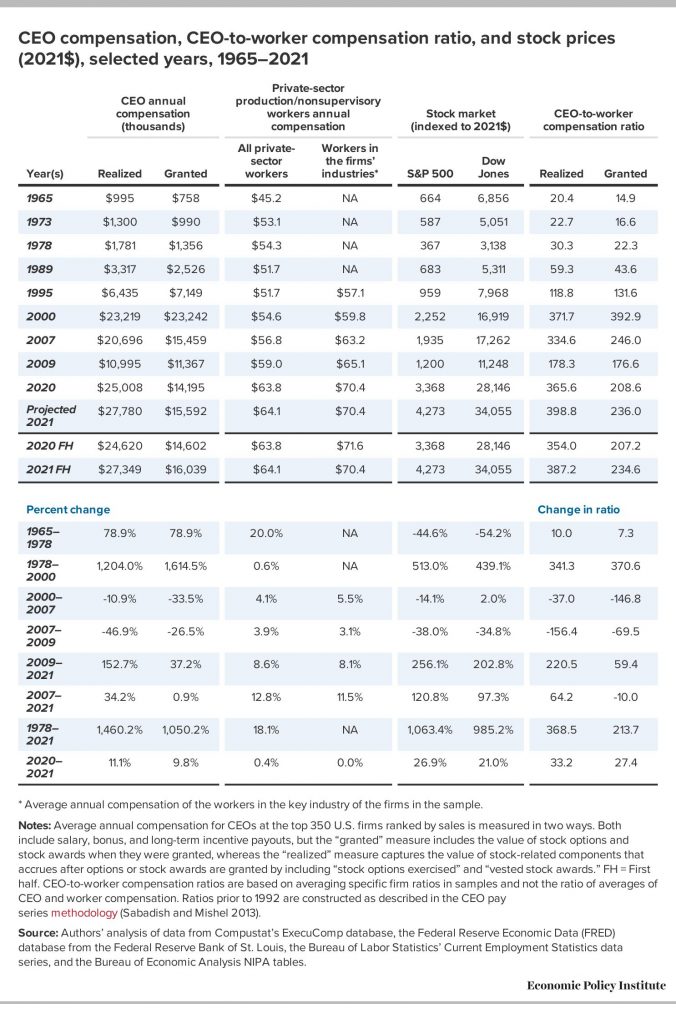

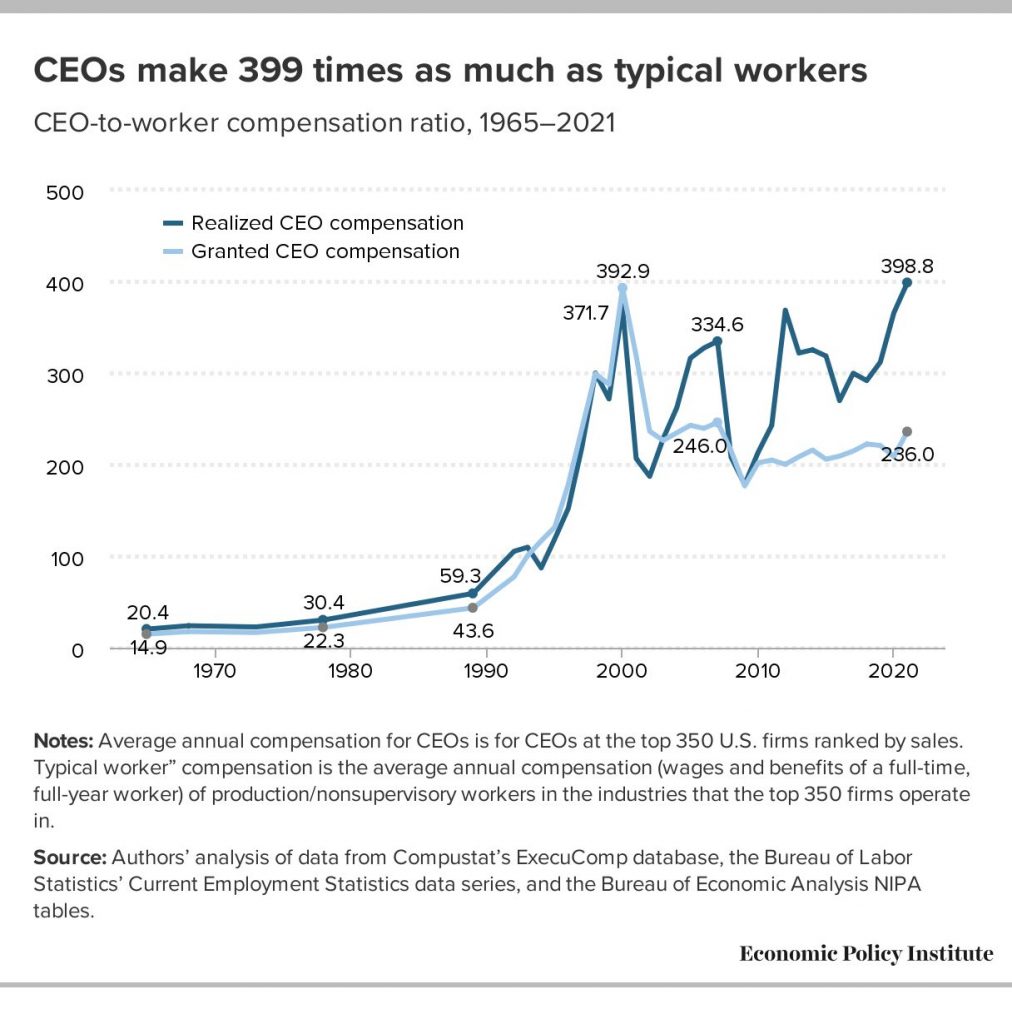

As rank-and-file benefits evolved, executive compensation soared. The CEO-to-worker pay ratio skyrocketed from 20-to-1 in 1965 to 123-to-1 in 1995. Stock options fueled this growth, igniting debates about income inequality that still rage today.

In 2021, the CEO-to-worker compensation ratio reached a staggering 399-to-1. To put this in perspective, in 1965, this ratio was just 20-to-1. The average S&P 500 CEO received total compensation of $18.3 million in 2021.

This compensation often comes in forms unavailable to regular employees:

- Large grants of stock options and restricted stock units

- Deferred compensation plans that allow for tax-advantaged savings beyond 401(k) limits

- “Golden parachutes” ensure soft landings even in cases of poor performance.

The justification for these packages often centers on the need to attract and retain top talent.

Financial Wellness: The New Frontier

As the responsibility for financial security has shifted more to employees, a new category of benefits has emerged: financial wellness programs. Employers are recognizing that financial stress can significantly impact productivity and overall well-being.

Currently, a lot of employers offer some form of financial wellness program. These can include:

- Budgeting workshops

- One-on-one financial counseling

- Tools for tracking spending and savings

- Education on topics like investing and debt management.

One particularly innovative benefit gaining traction is student loan repayment assistance. With the average student debt burden climbing rapidly, this benefit is especially appealing to younger workers.

The Power Players of the American Benefits World

Let’s pull back the curtain and examine the power players that influence every aspect of the USA employee benefits package. From government regulators to insurance giants, from retirement behemoths to tech disruptors, these entities form the backbone of the U.S. benefits system.

The Government Guardians

At the federal level, four key agencies stand out as the primary architects and enforcers of benefits policy:

- Department of Labor (DOL)

The DOL serves as the primary protector of worker rights, including those related to employee benefits. Its influence is far-reaching and profound:

- Enforces crucial legislation like the Employee Retirement Income Security Act (ERISA) and the Family and Medical Leave Act (FMLA)

- Key divisions like the Employee Benefits Security Administration (EBSA) and the Wage and Hour Division act as vigilant guardians of your rights

The department’s efforts ensure that employee benefits are secure, properly managed, and in compliance with federal law.

- Internal Revenue Service (IRS)

While most people think of the IRS solely in terms of tax collection, its role in the benefits world is equally crucial:

- Shapes the very structure of benefits through tax laws and regulations.

- Oversees retirement plans with stringent rules on contributions, distributions, and reporting.

- In 2020, collected $3.5 trillion in taxes and processed 240 million returns

The tax-advantaged nature of many benefits – from 401(k) contributions to Health Savings Accounts – is a direct result of IRS regulations.

- Health and Human Services (HHS)

HHS plays a pivotal role in shaping health benefits across the nation:

- Implements crucial provisions of the Affordable Care Act

- Oversees Medicare and Medicaid, which influence private insurance markets.

- 2023 budget: $1.7 trillion, underlining its massive influence on the healthcare system

Every time Sarah uses her health insurance or benefits from a preventive care provision, she’s interacting with a system heavily influenced by HHS policies and regulations.

- Equal Employment Opportunity Commission (EEOC)

The EEOC ensures that benefits programs don’t discriminate against employees:

- Enforces laws prohibiting discrimination in all aspects of employment, including benefits.

- Received 73,485 workplace discrimination charges in 2022

- Recently focused on regulations surrounding wellness programs

The EEOC’s work ensures that all employees have fair and equal access to benefits, regardless of age, gender, race, or other protected characteristics.

State-Level Sheriffs

While federal agencies set overarching policies, state-level regulators play a crucial role in shaping the benefits landscape at a more local level:

- State Insurance Commissioners

These officials serve as the primary regulators of insurance products within their states:

- Approve insurance rates and policy forms.

- Investigate consumer complaints.

- Enforce state insurance laws.

For example, California’s Department of Insurance is known for its rigorous rate review process for health insurance plans. State Labor Departments

These departments often implement and enforce state-specific labor laws, which can exceed federal standards:

- Oversee state-specific paid leave programs.

- Enforce state minimum wage laws.

- Implement state-specific worker protection regulations.

A prime example is New York’s Paid Family Leave program, which provides up to 12 weeks of paid leave, surpassing the unpaid leave mandated by the federal FMLA.

The Insurance Behemoths

The health insurance industry is dominated by a handful of large players, each wielding enormous influence:

- UnitedHealth Group

- The largest health insurer with a 14.1% market share

- 2022 revenue: $287.6 billion

- Covers 51 million members.

UnitedHealth’s size gives it significant bargaining power with healthcare providers, influencing the cost and availability of services for its members.

- Anthem (Elevance Health)

- The second-largest insurer, holding 11.8% of the market.

- Part of the Blue Cross Blue Shield Association

- 2022 revenue: $156.6 billion

Anthem’s association with Blue Cross Blue Shield gives it a unique position in the market, often offering a wide network of providers.

- Cigna

- Recently merged with pharmacy benefit manager Express Scripts

- Focusing on integrated health services

- 2022 revenue: $180.5 billion

Cigna’s merger with Express Scripts represents a trend toward vertical integration in healthcare, aiming to control costs by managing both insurance and pharmacy benefits.

- Aetna (CVS Health)

- Acquired by CVS Health, reshaping healthcare delivery.

- Pushing innovative benefit approaches

- CVS Health’s 2022 revenue: $322.5 billion

The CVS-Aetna merger represents a bold move to combine insurance, pharmacy, and direct healthcare delivery, potentially transforming how consumers access health services.

These insurance giants shape the entire healthcare landscape. Their decisions on coverage, networks, and reimbursement rates ripple throughout the system, affecting everything from hospital operations to individual treatment options.

The Retirement Titans

The world of retirement benefits is dominated by a few key players, each managing trillions of dollars in assets:

- Fidelity Investments

- The largest 401(k) provider with approximately 35% market share

- Assets under management: $4.5 trillion (2023)

- Known for its user-friendly interfaces and educational resources.

Fidelity’s dominance in the 401(k) space means its investment options and plan designs influence retirement outcomes for millions of Americans.

- Vanguard

- Pioneer of low-cost index funds

- Assets under management: $7.5 trillion (2023)

- Rapidly expanding its presence in the 401(k) market

Vanguard’s emphasis on low-cost investing has put pressure on the entire investment industry to reduce fees, potentially saving retirement savers billions over their lifetimes.

- Charles Schwab

- Recently acquired TD Ameritrade

- Assets under management: $7.05 trillion (2023)

- Expanding its retirement plan services

Schwab’s acquisition of TD Ameritrade has created a new powerhouse in the retail and retirement investing space, offering a wide range of services from basic 401(k) plans to complex wealth management.

The Tech Disruptors

Technology is rapidly transforming the benefits landscape, with several key players leading the charge:

- Workday

- Provides cloud-based HR and finance software.

- 2022 revenue: $5.14 billion

- Used by many large enterprises for benefits administration.

Workday’s integrated platform is changing how companies manage their workforce and benefits, offering real-time insights and simplified administration.

- ADP (Automatic Data Processing)

- A veteran in payroll and benefits administration

- Serves 920,000 clients globally.

- 2022 revenue: $16.5 billion

ADP’s vast client base gives it significant influence in shaping how companies, especially small and medium-sized businesses, approach benefits administration.

- Zenefits

- Disruptor in small business benefits administration

- Recently pivoted to become a Professional Employer Organization (PEO)

- Serves over 11,000 small and mid-sized businesses.

Zenefits represents a new breed of tech-forward benefits company, aiming to simplify and streamline benefits for smaller employers who might otherwise struggle to offer competitive packages.

The Thought Leaders

Several organizations play crucial roles in shaping benefits policy, research, and best practices:

- Society for Human Resource Management (SHRM)

- Membership: Over 300,000 HR and business executive members in 165 countries

- Provides education, certification, and advocacy for HR professionals.

- Publishes influential annual reports on benefits trends.

SHRM’s research and recommendations often set the standard for benefits practices across industries. When Sarah’s HR department considers new benefits offerings, they’re likely consulting SHRM resources.

- Employee Benefit Research Institute (EBRI)

- Non-partisan research organization focused on employee benefits.

- Conducts the annual Retirement Confidence Survey, a benchmark in the industry.

- Provides objective, in-depth analysis of benefits, trends and policies.

EBRI’s research often informs policymakers and industry leaders, indirectly influencing the benefits available to workers across the country.

- National Business Group on Health

- Represents large employers on health policy issues.

- Membership includes 440 large employers covering 55 million lives in the U.S. and globally.

- Advocates for employer interests in healthcare policy discussions

This organization’s lobbying and policy recommendations can significantly impact healthcare legislation and regulations, affecting the health benefits available to millions of workers.

Every benefit decision, from the structure of health plans to the availability of parental leave, is influenced by this ecosystem. Understanding these players and their roles empowers employees to navigate their benefits more effectively and advocate for their needs.

The Future of Work and Benefits: A Brave New World

Artificial Intelligence and Machine Learning are set to revolutionize benefits administration. Predictive analytics will flag potential health issues before they arise, while personalized benefit recommendations will be tailored to your lifestyle and needs. By 2031, the AI in HR market is projected to reach $14.8 billion, underscoring the rapid pace of this transformation.

Blockchain technology promises to bring security, efficiency, and decentralization to benefits. Picture a world where claims are processed in seconds, not weeks, and where your benefits follow you seamlessly from job to job through a decentralized platform.

Virtual Reality is poised to transform the often-dreaded open enrollment period into an immersive experience. Employees might soon step into virtual benefits fairs, test-driving different health plans in simulated scenarios. VR wellness programs could offer meditation sessions on virtual beaches, making self-care more engaging and accessible.

The Internet of Things (IoT) is blurring the lines between wearable devices and health plans. Your smartwatch might soon do more than count steps—it could feed real-time health data to insurers, potentially leading to usage-based insurance models that reward healthy behaviors. With the wearable medical devices market expected to reach $46.6 billion by 2025, this trend is only set to accelerate.

The Medicare for All Debate

A seismic shift looms on the horizon: Medicare for All. This proposal could save billions on national health expenditures and employer healthcare spending. But the implications are complex and far-reaching.

For employers, it could mean a reduced benefit administration burden, but also the loss of a key talent attraction tool. Employees might gain universal coverage regardless of employment status but could face longer wait times and less choice. Insurance companies would need to fundamentally reshape their business models, while healthcare providers might see simplified billing processes but potentially reduced reimbursement rates.

Alternative proposals are also on the table, including a public option and Medicare buy-in for older adults. The outcome of this debate will shape the future of American healthcare and employee benefits for decades to come.

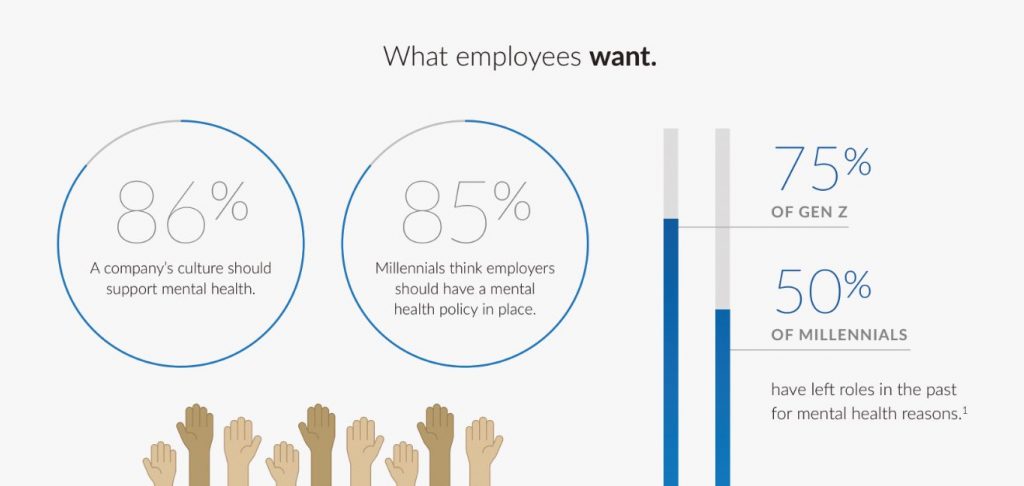

The Millennial and Gen Z Revolution

By 2030, millennials will make up 75% of the workforce, with Gen Z hot on their heels. These generations are redefining benefit priorities. Student loan repayment assistance, robust mental health support, and work-life balance benefits are no longer perks—they’re expectations.

Gen Z takes these demands even further, considering financial wellness programs non-negotiable and expecting hyper-personalized benefits. They’re also changing how benefits are communicated, demanding mobile-first, on-demand information about their options.

The Future Workplace

The future of work is remote, flexible, and deeply personal.

The gig economy continues to grow, driving the development of portable benefits models and increasing the role of Professional Employer Organizations (PEOs) as benefits hubs for freelancers.

Hyper-personalization is becoming the norm, with data analytics driving tailored benefit offerings. “Choose your own adventure” benefit models allow employees to customize their packages to their unique needs.

Even time off is evolving. Unlimited PTO policies are spreading, and sabbaticals are becoming powerful tools for talent attraction and retention.

As we look to the future, new benefit trends are emerging. Financial wellness programs are expanding beyond retirement to include emergency savings accounts and even cryptocurrency options in 401(k)s. Mental health support is moving front and center, with digital platforms and stress-reduction programs becoming standard offerings. The caregiving crisis is driving increased support for both childcare and elder care.

In this brave new world of benefits, the role of the government is also evolving. Debates around Universal Basic Income are moving from the fringe to the mainstream, while gig worker protections are becoming a legislative priority. As benefits become more personalized, data privacy is emerging as the next regulatory frontier.

The future of work and benefits in the USA is being written now, shaped by technological advancements, demographic shifts, and changing societal needs. As we navigate this evolving landscape, one question remains: How will your needs change, and what benefits can you imagine that don’t yet exist?